Latest Facts and News

- IRS tightens oversight on CNC approvals (Mar 2025): The IRS now requires stricter managerial approval for accounts marked Currently Not Collectible (CNC), ensuring thorough investigations and adherence to the updated March 2025 IRM standards.

- Monthly CNC tracking now mandatory: The IRS will now track all CNC closures through monthly and quarterly reports, including the TDA Monthly Report and CNC-149. These reports monitor not just case counts but total dollar volumes removed from collection activity.

- ICS analysts gain more CNC case control: As of 2025, IRS Quality Analysts and the Inventory Delivery System (IDS) are authorized to shelve or recess qualifying CNC cases, helping reduce IRS backlog and reassign resources more efficiently across business units.

When you’re already watching every dollar just to keep the basics going, getting an IRS tax collection notice can feel like the final blow. Back tax debt can become a constant source of stress, fear, and sleepless nights for you. The idea of collection actions, wage garnishments, or levies only adds to the pressure.

On top of that, interest builds up steadily, making what was once a manageable tax bill feel impossible overnight. The IRS adds a failure-to-pay penalty of up to 25% of what you owe and charges 7% interest on unpaid taxes. That means the longer you wait, the deeper the hole gets.

Fortunately, relief options exist for those in severe financial hardship. Through the Currently Not Collectible (CNC) status, you can get temporary relief from aggressive IRS actions.

But getting that status isn’t automatic, and not everyone qualifies. That’s why it’s important to understand how back tax debt non collectible relief works.

In this guide, we’ll explain what “IRS Currently Not Collectible (CNC)” status really means, who qualifies, and how it can provide temporary relief to help you regain financial stability.

What is Currently Not Collectible Status?

The IRS Currently Not Collectible (CNC) status is a temporary tax debt relief option when you cannot afford to pay your tax debt without sacrificing basic living expenses.

When the IRS grants CNC status, it halts active collection efforts, such as wage garnishments, bank levies, and asset seizures, but the debt remains.

Key Features of CNC Status

- Stops IRS collection actions, like wage garnishments, bank levies, and asset seizures.

- Does not eliminate tax debt. Interest and penalties continue accruing as normal.

- The IRS may file a federal tax lien for debts exceeding $10,000, impacting credit scores.

- You must provide detailed financial information, and the IRS periodically reviews your status.

If you think that Currently Not Collectible status might be an option, let’s see if you qualify.

Eligibility Criteria for CNC Status

Before applying for Currently Not Collectible (CNC) status, it’s important for you to understand when this option is appropriate. CNC status is typically granted when other relief options, such as an Offer in Compromise (OIC) or an Installment Agreement, are not viable due to severe financial hardship.

To qualify, you must prove that paying taxes would leave you unable to cover essential expenses.

Financial Hardship Requirements

The IRS evaluates a taxpayer’s income-to-expense ratio to determine back tax debt non-collectible status eligibility. If basic living expenses exceed income, CNC status may be granted.

The IRS considers the necessary expenses that are given below.

- Rent or mortgage payments

- Utilities (electricity, water, gas)

- Groceries

- Medical expenses

- Transportation costs

| Example: If your total monthly income is $2,500 but your necessary expenses are $2,700, you may qualify for back tax debt non collectible status. |

Documentation Needed

To apply for CNC status, you must submit IRS Form 433-F and provide financial statements showing you cannot afford payments. The required documents typically include:

- Bank statements (checking and savings accounts)

- Pay stubs or proof of income (for the last 3 months)

- Monthly bills and living expenses

- Rent/mortgage statements

- Utility bills (electricity, water, gas, internet, phone)

- Medical expenses receipts, and insurance premiums

- Asset details (such as home value and vehicle information)

- Credit card statements

- Other loan statements (student loans, personal loans, etc.)

How to apply for Currently not Collectible Status?

Before the IRS can mark your tax debt as non collectible, you must provide detailed financial information that proves you’re unable to pay. This process begins with submitting Form 433-F and supporting documents.

Complete IRS Form 433-F

To begin, you must complete IRS Form 433-F, which helps the IRS evaluate your financial situation and determine if you qualify for non-collectible status.

Step 1: Gather financial documents

Collect all the documents listed in the “Documentation Needed” section above.

Having these documents readily available will make the form completion process faster and smoother.

Step 2: Complete IRS Form 433-F

Correctly filling out IRS Form 433-F is crucial for applying for Currently Not Collectible (CNC) status. Here is a step-by-step breakdown of each section.

NOTE: Make sure you include your spouse and business details if applicable.

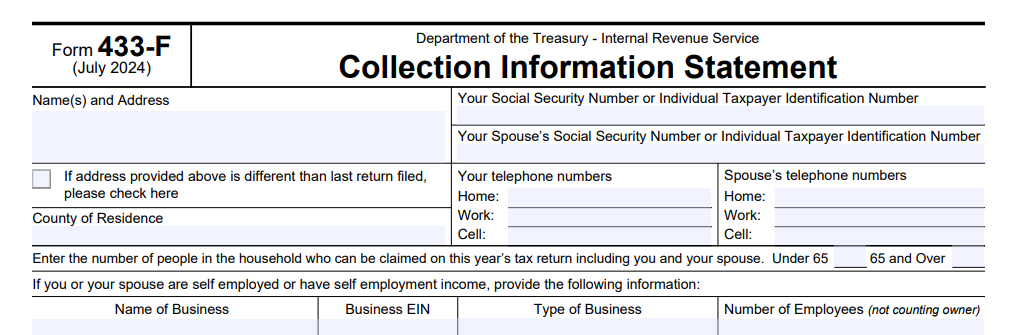

Section 1: Fill Out Personal Information

| Field | What to Enter |

| Name & Address |

Your full legal name and current address (If your address has changed, check the box provided.) |

| Social Security Number (SSN) | Your SSN and your spouse’s SSN (if applicable) |

| Phone Numbers | Home, work, and cell phone numbers |

| Household Size | Number of dependents in your household |

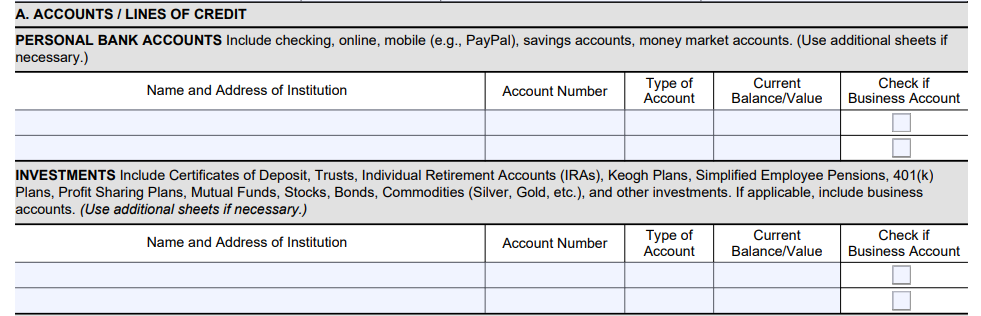

Section 2 (A): List Bank Accounts & Investments

Here, you need to report your personal and business financial accounts, such as those given in the section below:

- Checking & Savings Accounts (include balance amounts)

- Online Payment Accounts (PayPal, Venmo, Cash App, etc.)

- Retirement Accounts (IRA, 401(k))

- Investment Accounts (Stocks, Bonds, Mutual Funds, etc.)

| Field | What to Enter |

| Bank Name & Address |

Name of the financial institution (List all active accounts.) |

| Account Number | Full or last 4 digits of the account |

| Type of Account | Checking, savings, investment |

| Current Balance | The amount in the account today |

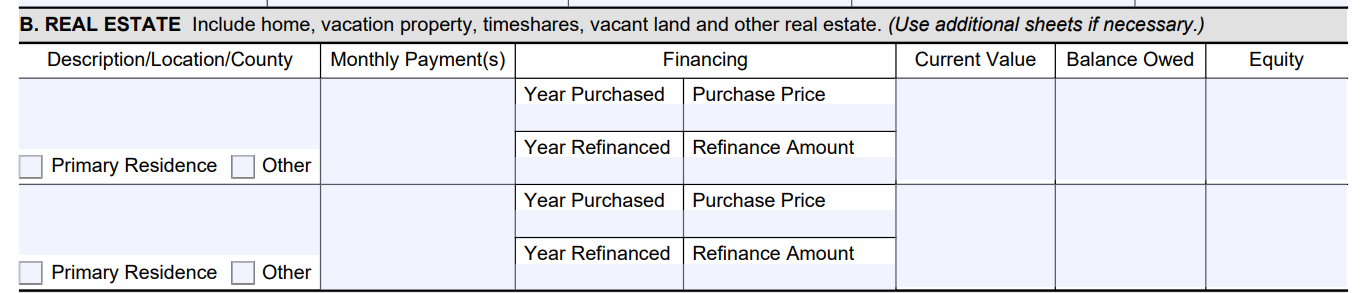

Section 3 (B): Report Real Estate & Property Assets

Here, list any real estate you own, including:

- Primary Residence

- Rental Properties

- Vacation Homes or Land

| Field | What to Enter | Notes |

| Property Description & Location | Address of the property | Be specific about the location. |

| Monthly Mortgage Payment | Your current payment amount | Include tax & insurance payments. |

| Current Property Value | Estimated market value | Use a real estate website or appraisal. |

| Loan Balance | How much do you owe | List the remaining balance on your mortgage. |

| Equity | Market value minus loan balance | If negative, list “0.” |

Section 4 (C): List Other Assets

- Vehicles (Cars, Trucks, Motorcycles, Boats, RVs, etc.)

- Business Assets (Tools, Equipment, Inventory, etc.)

- Whole Life Insurance Policies (if applicable)

| Field | What to Enter | Notes |

| Description | Make, model, and year | Example: “2018 Toyota Camry.” |

| Monthly Loan Payment | The amount you pay for the asset | If fully paid, enter “0.” |

| Current Value | Estimated resale value | Use Kelley Blue Book (KBB) for cars. |

| Loan Balance | Amount still owed | If none, enter “0.” |

| Equity | Value minus remaining balance | If negative, enter “0.” |

| NOTE: If your assets are fully paid off, the IRS may view them as payment sources for your tax debt. |

Section 5 (D): Business Information – List Credit Cards & Other Debt

Report all outstanding debts, including:

- Credit Cards (Visa, MasterCard, Store Cards, etc.)

- Lines of Credit & Personal Loans

| Field | What to Enter |

| Type of Credit | Credit card or loan type |

| Credit Limit | Maximum available credit |

| Balance Owed | Current balance |

| Minimum Monthly Payment | Your required payment |

| NOTE: The IRS considers minimum debt payments when determining CNC eligibility. |

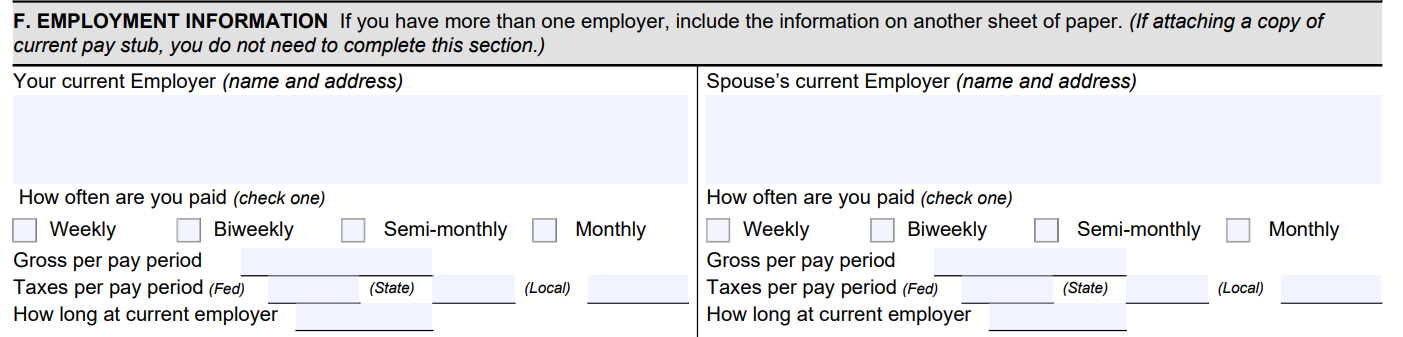

Section 6 (F): Report Employment Information

If you are employed, provide details about your job:

- Employer’s name & address

- How often are you paid (weekly, bi-weekly, monthly)

- Gross income per pay period

- Taxes deducted (Federal, State, and Local)

- How long have you been with the employer

- If unemployed, write “Unemployed” in the employer section.

| NOTE: If you are self-employed, you must provide a profit and loss statement to verify your earnings. |

Section 7 (G): Report Income

List all income sources, like:

- Wages & salary

- Unemployment benefits

- Pension & social security

- Rental income

- Child Support & Alimony

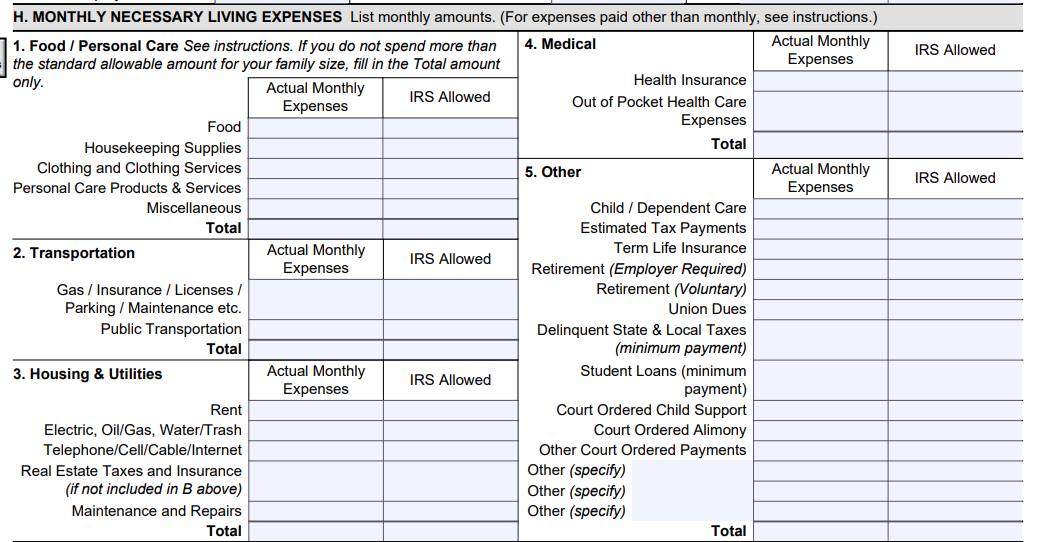

Section 8 (H): Report Necessary Living Expenses

The IRS compares your expenses to national standards before approving CNC status.

- Rent or mortgage

- Utilities (electric, gas, water, internet, phone, etc.)

- Food & personal care

- Transportation (gas, insurance, public transport, etc.)

- Medical Expenses & health insurance

| NOTE: If your expenses exceed IRS standards, you may need to provide proof of necessity. |

Lastly, sign and submit the Form

Before submitting:

- Double-check for errors.

- Sign and date the form

- Attach supporting documents (bank statements, bills, pay stubs, etc.)

- Submit via mail or fax (based on IRS instructions)

Step 3: Contact the IRS or hire a tax professional.

Contact the IRS at 1-800-829-1040 for queries. Filing Form 433-F is complex and is the first step; getting IRS approval is the real challenge. One mistake can lead to IRS rejections or delayed approvals and put you back into collections.

Instead of solving this alone, let Salinger Tax Consultants handle the process. We carefully review your financial situation, complete Form 433-F accurately, and speak directly with the IRS on your behalf. Our experts help reduce errors, save time, and maximize your chances of CNC approval.

Common Mistakes to Avoid

- Underreporting side income: Freelance gigs, cash jobs, or rental income often go unreported. The IRS cross-checks data; missing this can flag your account for audit or denial.

- Submitting outdated financial info: Using old pay stubs or bank statements makes it look like you’re hiding current income. Always submit the most recent documents to reflect your actual financial hardship.

- Ignoring monthly expense limits: The IRS has set “allowable living expenses.” If you list costs that exceed those limits (e.g., luxury car payments), your CNC request may be denied.

- Leaving out shared household income: If you live with a partner or relative who contributes to bills, the IRS expects you to include their income. Many people skip this and risk rejection.

- Skipping asset details: Not reporting items like a second car, crypto holdings, or savings accounts (even if they seem minor) can be seen as dishonest.

- Failing to update financial details: If your income improves, CNC status on back taxes may be revoked.

Pros and Cons of CNC Status

Before you consider going into Currently Not Collectible (CNC) status, it’s important to weigh how it could help or hurt you in both the short and long run. The table below breaks down what you can realistically expect so you can decide if the CNC status aligns with your financial goals.

| Factor | Pros | Cons |

| IRS Collections | Stops wage garnishments, bank levies, and property seizures. | The IRS may file a federal tax lien, affecting your credit score. |

| IRS Communication | No more IRS harassment, letters, or collection calls. | You must stay in contact with the IRS and update financial changes. |

| Financial Relief | No immediate tax payments are required, allowing time to recover. | Interest and penalties continue to grow, increasing the total owed. |

| Eligibility Requirement | Available when you prove financial hardship | The IRS will closely examine your finances and may request proof. |

| Tax Debt Status | The IRS pauses active collection efforts while in CNC. | CNC does not erase tax debt—it remains owed until paid or forgiven. |

| Future IRS Review | If financial hardship continues, CNC status can be renewed. | If your income increases, the IRS can remove CNC status anytime. |

| Credit Impact | No immediate impact on credit scores, unlike bankruptcy. | A federal tax lien can damage your ability to get loans or credit. |

| Long-Term Consequences | CNC status can buy time to explore better tax relief options. | If the IRS determines you can pay, CNC status may be denied or revoked. |

IRS uncollectible status statute of limitations

If your tax debt is Currently Not Collectible (CNC) status, the IRS has a 10-year statute of limitations on collecting tax debt. This means the IRS has exactly 10 years from the assessment date to collect what you owe. After that, the debt is legally erased.

However, if your financial situation improves, the IRS can restart collection efforts against you before the deadline.

IRS uncollectible status tax lien, and Notice of federal tax lien

Even if you qualify for CNC status, the IRS can still file a federal tax lien against you. A tax lien is a legal claim on physical assets such as your home and car.

If your tax debt is over $10,000, a lien is almost guaranteed. While the IRS won’t seize your assets while in CNC status, the lien can hurt your credit and make it harder to get loans. The best way to remove a lien is to pay the debt, settle with an Offer in Compromise, or wait until the IRS’s 10-year collection window expires.

Alternatives to Back Tax Debt Non Collectible Status

While the CNC status provides temporary relief, it’s important to consider all available options to address your tax debt situation. Here are some alternatives that might better suit your circumstances:

Offer in Compromise (OIC)

The IRS Offer in Compromise program helps you reduce your tax burden by allowing you to pay a smaller, agreed-upon amount. It gives you a chance to pay less than what you originally owed.

- The IRS has strict qualification requirements, including proving that full payment would create significant financial hardship.

- If approved, you can pay off your tax debt for a reduced amount in a lump sum or structured payments.

|

Example: Let’s say you’re a small business owner who owes $80,000 in back taxes after the pandemic forced you to close down. Your only income is a part-time job making $2,000 monthly, and you have minimal assets. With Peter Salinger’s help, they can submit an Offer in Compromise, showing they can only afford $10,000 in total. The IRS may accept a settlement of their tax debt and save them $70,000. |

Installment Agreements

If CNC status isn’t an option for you, you can negotiate an IRS installment agreement to pay your debt over time. These agreements allow you to make manageable monthly payments instead of paying in full immediately.

- Payments are made directly to the IRS until the debt is fully paid.

- No IRS levies or garnishments occur if payments are on time.

|

Example: If you’re a software developer with $50,000 in back taxes, making $7,500 per month, and can’t qualify for CNC or OIC, Salinger Tax Consultants can help you set up a $500 installment agreement, avoiding IRS collections while keeping payments affordable. |

IRS Tax Hardship Programs

If you can pay some but not all of your tax debt, you may qualify for an IRS hardship program, which:

- Reduces your required monthly payments.

- Prevents collections like wage garnishments.

- Allows partial payments until your financial situation improves.

| Example: If you’re a retiree on Social Security with $20,000 in tax debt and cannot afford CNC status but can pay $50 monthly, we can help negotiate a reduced IRS hardship payment legally, stopping collections while keeping costs affordable. |

Which Tax Relief Option Is Best for You?

| Option | Best for Taxpayers Who… | Key Benefit |

| Currently Not Collectible (CNC) | Cannot afford any payments without financial hardship (must show full financial proof) | IRS stops collections, but interest accrues |

| Offer in Compromise (OIC) | Want to settle for less than what they owe (must prove inability to pay full debt) | IRS may reduce the total tax debt |

| Installment Agreement | Can afford monthly payments but need time (must show consistent income) | Avoids IRS collections while paying overtime |

| Innocent Spouse Relief | We were unaware of a spouse’s tax fraud/mistake | Removes liability for unfair tax debt |

| Bankruptcy (Chapter 7/13) | Have tax debt older than 3 years and meet specific legal conditions | May discharge tax debt permanently |

| IRS Hardship Program | Can pay a small amount, but need relief (must submit detailed financial documents) | Reduces required IRS payments |

Note →

These programs are not guaranteed. You must apply with complete and accurate financial information, and the IRS will decide which relief fits your situation best. Always consult a tax professional to improve your chances.

Get Expert Tax Solutions Today with Salinger Tax Consultants

Dealing with the IRS is stressful, frustrating, and time-consuming, especially when you’re already struggling financially. The IRS doesn’t make it easy to qualify for back tax debt non collectible status or other tax debt relief programs. A single mistake on Form 433-F could mean delays, denials, or even IRS enforcement actions like wage garnishments and bank levies.

This is where Salinger Tax Consultants comes in.

- You don’t have to sit on hold for hours or decipher IRS jargon. We handle ins and outs for you.

- Our expert team ensures that your CNC application is accurate and complete, reducing the risk of rejections.

- If CNC isn’t the best fit, we’ll explore other relief options, including Offer in Compromise and Installment Agreements.

|

Let us take the stress out of your taxes. See why our clients trust us! “Peter was able to get late payment penalties waived for me. He helped me figure out how much I owed in taxes and he was able to get me into a monthly payment plan — Elissa S” |

You’ve already been through enough stress. Let us take this burden off your shoulders. Contact us today, and we’ll handle the IRS for you.