Form 843 is the IRS form used to remove IRS penalties, reduce interest, or request refunds when the IRS charges you incorrectly. The problem is not the form itself but misunderstanding the IRS Form 843 instructions, which leads many valid claims to fail quietly. Taxpayers often know they qualify for relief but do not know how to present it to the IRS.

In this blog, we will break down the IRS Form 843 instructions, explain when the form works, and show how to file it correctly so your request gets considered.

Understanding Form 843: What is it, and When Should You File?

Form 843 helps you request a refund or an abatement for certain IRS charges and is called the “Claim for Refund and Request for Abatement.”

In IRS terms, “refund” and “abatement” are not the same action. A refund asks the IRS to return money already paid on the account. An abatement means requesting the IRS to reduce or remove an assessed charge you have not paid. Form 843 exists because many claims do not belong on an amended return. The IRS also says you should not use Form 843 to amend a previously filed income or employment tax return. So, before you write anything, confirm that Form 843 fits your issue under the current IRS Form 843 instructions.

What Form 843 Cannot Be Used For?

Form 843 does not fix regular income tax overpayments on Form 1040. If you need to change amounts reported on Form 1040 series returns, the IRS points you to Form 1040-X instead. Form 843 also does not let employers adjust FICA, RRTA, or income tax withholding. Employers generally must use the “X” form that matches the original employment return, such as Form 941-X. If an employer can correct the issue, the IRS expects that correction process. Form 843 also does not cover certain fee refunds that many people assume it covers. The IRS instructions say not to use Form 843 for taxpayer agreement fees, offer-in-compromise fees, or lien fees. If your issue involves those fees, Form 843 will not help. For some excise tax refunds, the IRS instructions point to Form 8849 for certain excise tax refund claims. This is why the IRS Form 843 instructions matter more than online shortcuts.

Eligibility for Penalty Relief: The 3 Key Grounds

Most penalty relief claims fall into three legal lanes, and you must pick the lane that fits.

- Reasonable cause: Serious illness, disasters, and missing records can support this ground, but facts and timing must line up.

- Statutory exception: his ground depends on the specific penalty and the exact facts in your case.

- IRS error or delay: It matters most for limited interest relief cases.

When you use the IRS Form 843 instructions correctly, you match your facts to the allowed ground instead of guessing.

| Explore : Types of IRS Tax Relief Forms |

Step-by-Step: IRS Form 843 Instructions Line-by-Line

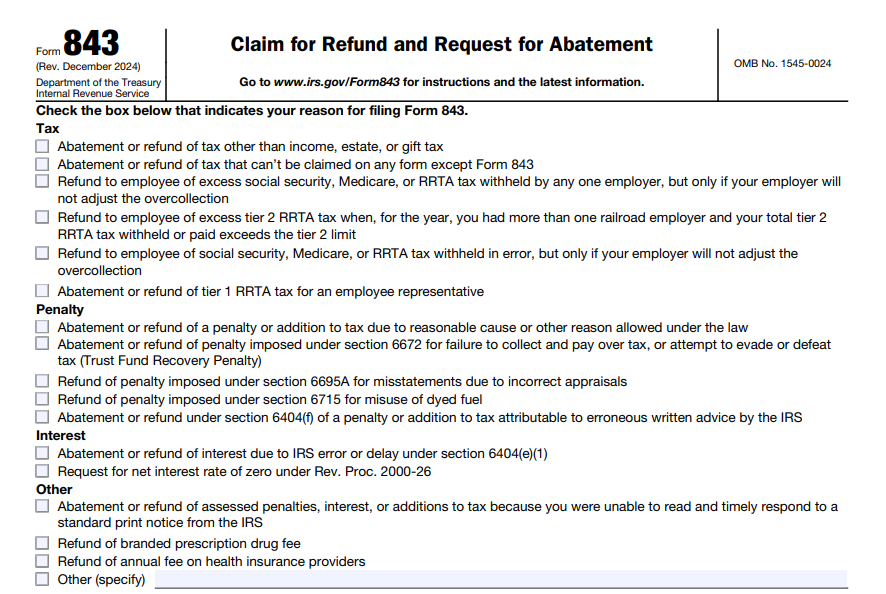

The IRS wants you to check one reason box at the top of Form 843, and the instructions say not to check more than one. If you check the wrong box, the IRS may route your claim to the wrong place.

Top Section: Checking the Right Box

The top checkboxes tell the IRS what you want and why you qualify. Here is the list of main groups you have:

- Tax refund or tax abatement requests for specific non-income taxes.

- Employee refunds for excess Social Security, Medicare, or RRTA withholding.

- Penalty relief requests, including standard penalties and special code sections.

- Interest relief requests, but only for limited reasons that the law allows.

- Special “other” requests, including disability-related timing issues and certain fees.

If you want Penalty Abatement, you must select the penalty box that matches your claim reason. The form also includes a box tied to section 6672, which covers the Trust Fund Recovery Penalty (TFRP). That checkbox has extra rules later, and you should not treat it like a normal late-filing penalty. Some checkboxes apply only to employees, not employers. For example, employees can request a refund of excess Social Security or Medicare withheld by one employer, but only when the employer will not adjust the overcollection. If you miss that condition, the IRS can deny the claim even if you feel the withholding looked wrong.

For interest relief, the form includes a checkbox for IRS error or delay under section 6404(e)(1). This option does not cover every sad situation, since the law limits when the IRS can remove interest.

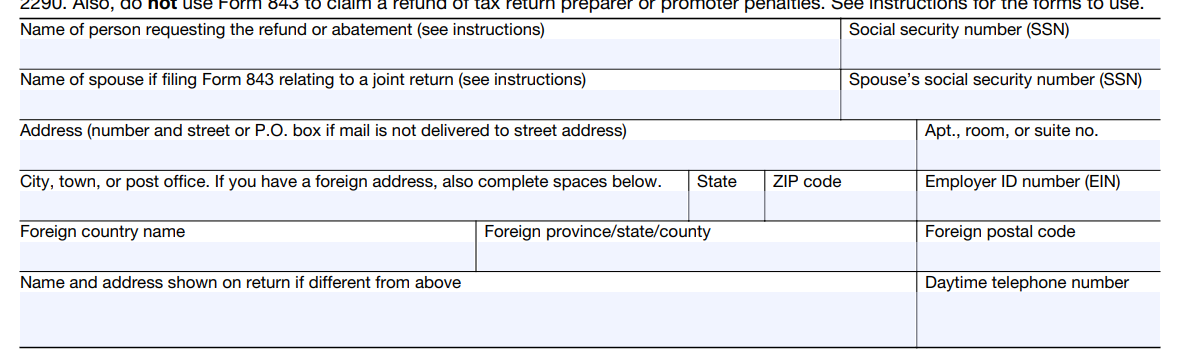

Section 1: Identification and Tax Period

Enter your name exactly as the IRS shows it on the related account or return. Enter your SSN, ITIN, or EIN, depending on who files the claim. If the matter involves a joint return, you must keep both names consistent throughout.

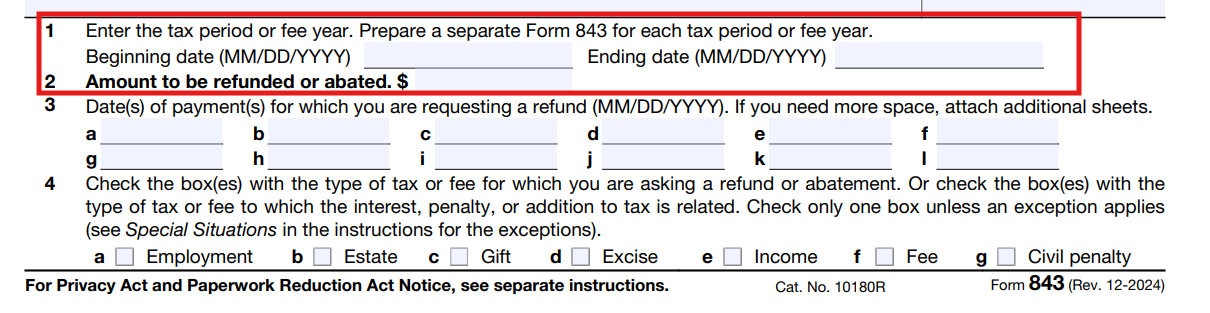

Line 1 asks for the tax period using a beginning date and ending date format. Many claims require separate forms for separate tax periods, and mixing years often creates delays.

Line 2: The Amount to be Refunded or Abated

Line 2 asks for the exact dollar amount you want refunded or removed. Do not estimate this number, since the IRS expects a clear computation later. If you want a refund, payment history matters because the IRS cannot refund what you never paid. If you want an abatement, the amount should match the assessed charge you want reduced.

Line 3–6: Identifying the Tax, Return, and Penalty

Line 3 asks for payment dates when you request a refund, so list each payment date you made. If you paid in multiple chunks, you should list every date clearly on the form or in an attachment.

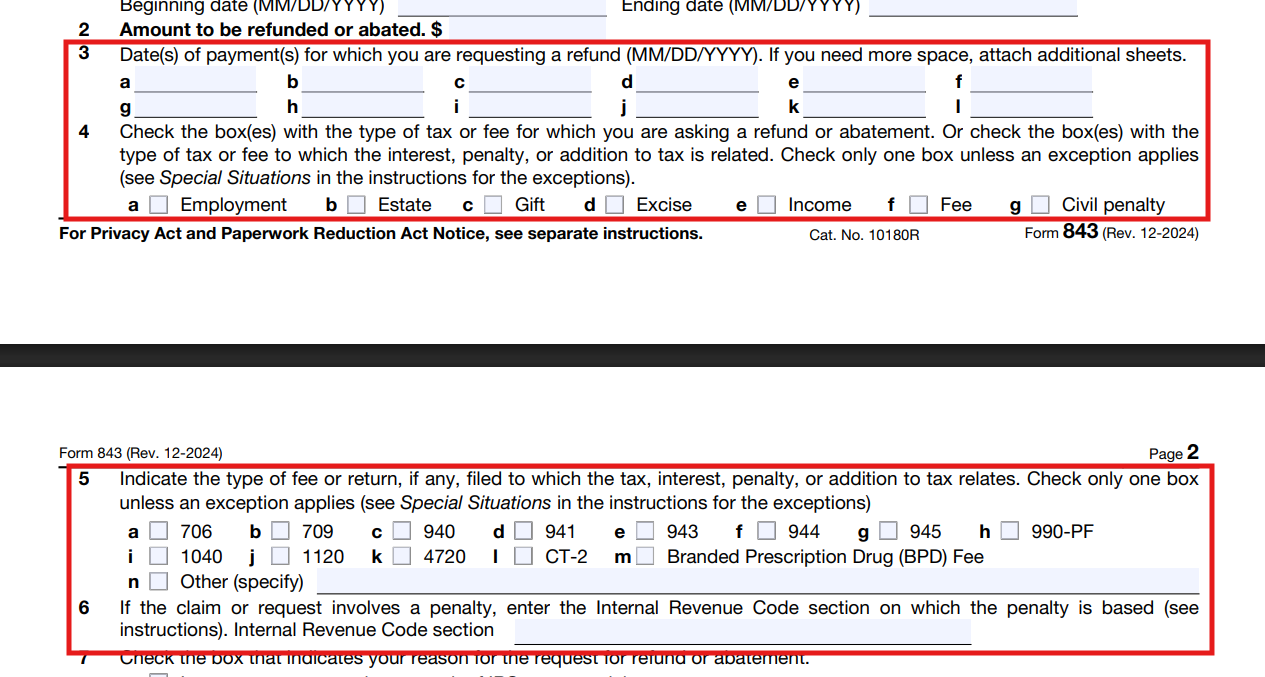

Line 4 asks for the type of tax or fee, like employment, excise, income, or civil penalty. Line 5 asks for the related return type, like Form 941 or Form 1040, depending on the issue. These boxes matter because the IRS routes claims based on tax type.

Line 6 is critical for penalty claims, since it asks for the code section tied to the penalty. You can usually find that code on your IRS Notice of Assessment, so use that exact reference instead of guessing.

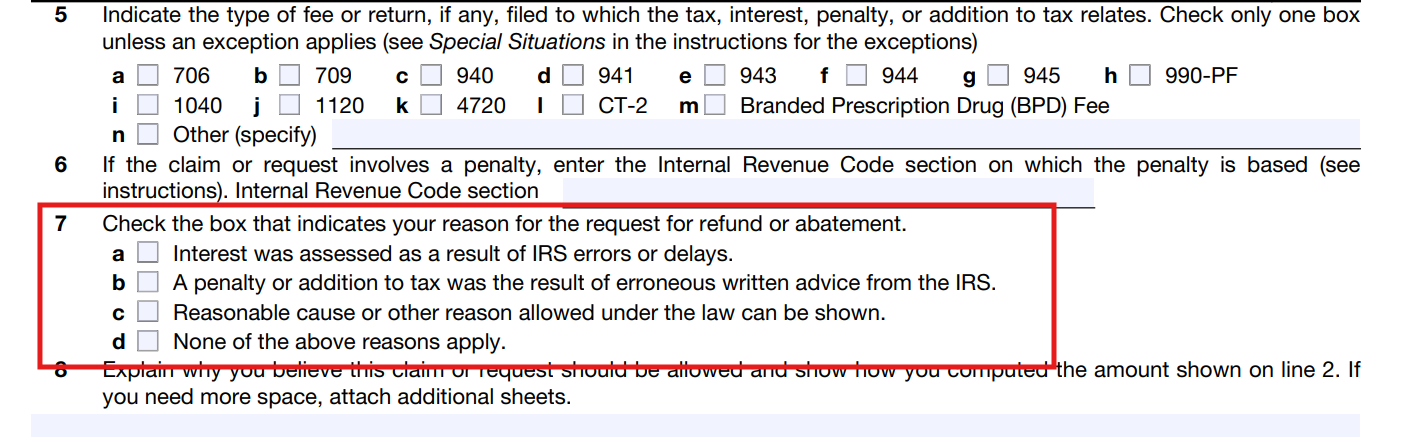

Line 7: The Crux of the Claim – Your Explanation

Line 7 wants you to pick the legal reason for your request, and the IRS wants one box checked. If none of the first three reasons fit, the IRS tells you to check box “d.” It matters because the IRS uses this choice to judge what proof they expect next. Here is what each line 7 box really means under the current IRS Form 843 instructions.

- Box (a) means you want interest relief because IRS errors or delays caused it. This box connects to section 6404(e)(1), and the IRS limits when it applies.

- Box (b) means the penalty came from erroneous written IRS advice you relied on. The IRS requires specific documents for this.

- Box (c) means you can show Reasonable Cause or another allowed reason under the law. This is the most common option for everyday penalty relief.

- Box (d) means none of the above fit, and you still have a lawful reason. If you use this box, your line 8 explanation must stay extra clear.

If you file a penalty claim based on written advice, the IRS only allows it when certain timing rules are met. The IRS says the request must be within the period allowed to collect the penalty, or you must have paid within the period allowed to claim a refund.

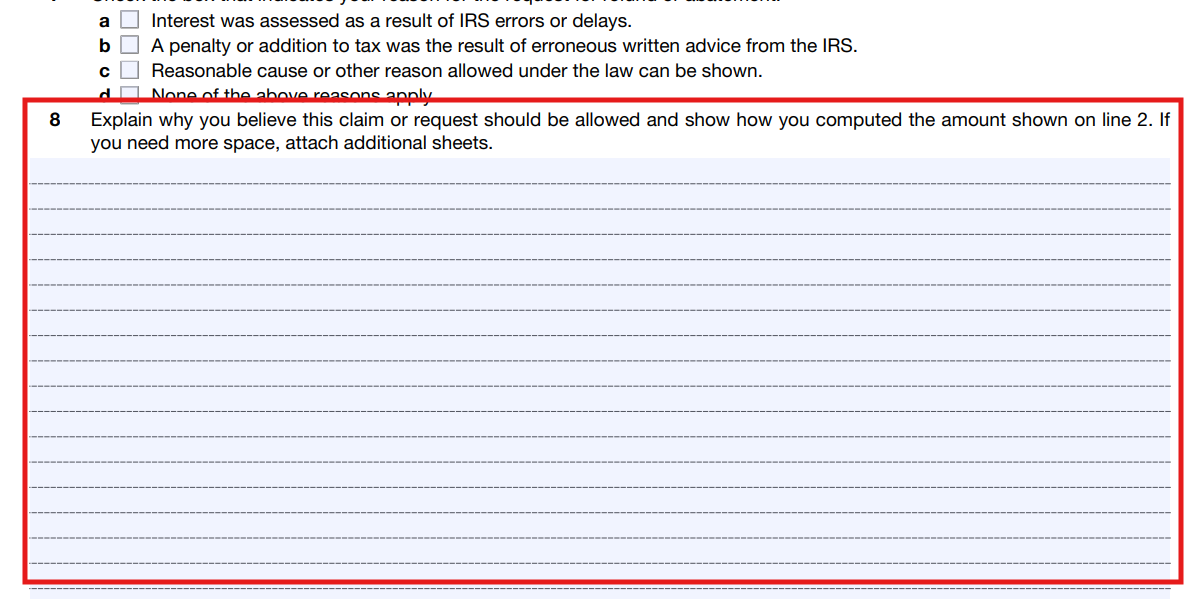

Line 8: The IRS Wants Your Proof

On line 8, the IRS tells you to explain in detail, show your computation, and attach supporting evidence. If you add extra pages, the IRS wants your name and SSN, ITIN, or EIN on every sheet.

A strong line 8 reads states what happened, when it happened, what you did, and what stopped you. Then you show what changed and how fast you fixed the problem once you could. This is a good moment to reread the IRS Form 843 instructions before you write. When people lose, they usually lose on line 8.

Signature Rules You Must Follow

If Form 843 relates to a joint return, both spouses must sign the form. If a corporation files, an authorized corporate officer must sign and include their title. If an estate or trust files, the fiduciary must sign. If a paid preparer files Form 843 for you, they must sign and complete the preparer area. The IRS also says a preparer who did not charge you should not sign. These small details matter under the IRS Form 843 instructions.

Submitting Your Claim: Where Do I Mail Form 843?

Mailing your Form 843 depends on why you file and what the claim involves. The IRS publishes a “Where To File” chart, and you should follow that chart instead of guessing. If you need to mail Form 843 in response to an IRS notice, you send it to the return address on that notice. If you file for penalties or most other reasons not listed in the special chart, you send it to the service center where you would file a current-year return for that tax type. If you are a nonresident alien requesting a refund of Social Security or Medicare withheld in error, the IRS says to use the address and rules in Pub. 519.

What to Attach to Form 843?

Attachments should match your checkbox and your story. The IRS Form 843 instructions want you to support your claim with evidence. These attachments often make sense in real cases:

- The IRS notice that shows the penalty or interest, especially if it lists the code section.

- Your payment proof, if you request a refund of something already paid.

- For employee FICA or Medicare issues, the IRS says you must attach a W-2 copy and, if possible, an employer statement showing what they repaid or claimed.

- For Trust Fund Recovery Penalty (TFRP) refund claims, the IRS requires that you first pay the portion tied to one employee or one transaction, depending on the type.

- For written advice claims, attach your written request, the IRS’s written advice, and any adjustment report that ties the penalty to that advice.

Maximizing Success: Insider Strategy for 843 Form Instructions

Most denials happen for bland reasons. The form goes to the wrong address, the tax period looks unclear, or the explanation lacks proof. Professional help becomes important when the situation gets complex. Large penalties, multiple years, payroll tax issues, or a Trust Fund Recovery Penalty (TFRP) can trigger rules that are easy to miss and hard to fix later. Salinger Tax Consultants focuses on these exact problem cases and reviews Form 843 claims before small mistakes turn into permanent losses. An expert consultation can confirm whether your claim stands strong or needs correction before the IRS decides for you.

The First-Time Penalty Abatement (FTA) vs. Form 843

First-Time Penalty Abatement (FTA) can feel easier, but in some cases, the IRS may grant FTA over the phone, and you may not need Form 843. Still, if you already paid a penalty and want money back, a Form 843 claim often makes more sense because you need a formal refund request.

What Happens After You File?

After you file, the IRS processing times move slowly, and follow-up mail can take months. If the IRS denies your claim, you may have appeal and court options depending on the type of denial. The outline also notes the “six-month rule,” where court review can become available if the IRS does not act. Your deadlines still matter, even when the IRS moves slowly. The IRS states the general refund claim deadline as three years from the date you filed the original return, or two years from the date you paid, whichever is later. That general rule is the Statute of Limitations that protects both sides, so track it carefully.

Fix IRS Penalties With Salinger Tax Consultants

IRS penalties do not fade with time, and one wrong move can lock them in permanently. Salinger Tax Consultants steps in before the damage becomes final by reviewing your facts, rebuilding your explanation, and filing Form 843 the way the IRS actually expects to see it. If the penalty scares you now, imagine it growing with interest later.

Contact us today and stop the problem before it hardens into a balance you cannot undo.

FAQs

Yes, in some situations. You can request an FTA by phone, but Form 843 helps when you have already paid the penalty and want a refund or when the IRS asks for a formal claim. Follow the current filing rules in the official instructions.

In most cases, you must file within three years from the date you filed the original return or within two years from the date you paid, whichever is later. Some special exceptions can apply, so confirm your exact deadline before mailing.

A letter can work for some penalty requests, especially simpler ones, but Form 843 gives the IRS a standardized claim with the exact fields they want. That usually reduces back-and-forth and prevents routing issues when the IRS needs the request on record.

You must mail Form 843. The IRS does not provide an e-file option for this form, so the delivery method matters. Use a trackable mailing service and keep copies of everything you send, including attachments, in case you need proof later.

If the IRS issues a formal notice of claim disallowance, you may have the right to go to court. If six months pass without IRS action, you may also gain court rights in certain refund claim situations. Keep your mailing proof and dates.

If you are responding to an IRS notice, mail Form 843 to the return address printed on that notice. If you are not responding to a notice, mail it to the service center where you would file a current-year return for that tax type.

No, this happens often. The IRS may want your request on Form 843 so it routes to the correct unit and includes the required identifying details. When the IRS tells you to use the form, comply and restate your facts cleanly on line 8.

Start with your employer, because the IRS expects the employer to correct withholding when possible. If the employer will not adjust it, Form 843 may help. The IRS also points nonresident aliens to Pub. 519 for extra rules and required documents.

The IRS can abate interest, but only in narrow cases tied to IRS errors or delays in managerial or ministerial acts. Personal hardship alone usually does not qualify. Interest abatement also applies only to certain taxes, and it does not apply to many employment tax cases.